Re-published with permission from the Financial Times, the original article can be found here. The writer is co-chief investment officer for sustainability at Bridgewater Associates.

The rush by investors of all stripes to prioritise environmental, social and governance goals has raised speculation of an emerging bubble in favoured stocks.

But the shift to ESG appears to be still in its early innings. Investor positioning in sustainable equities is not yet overextended.

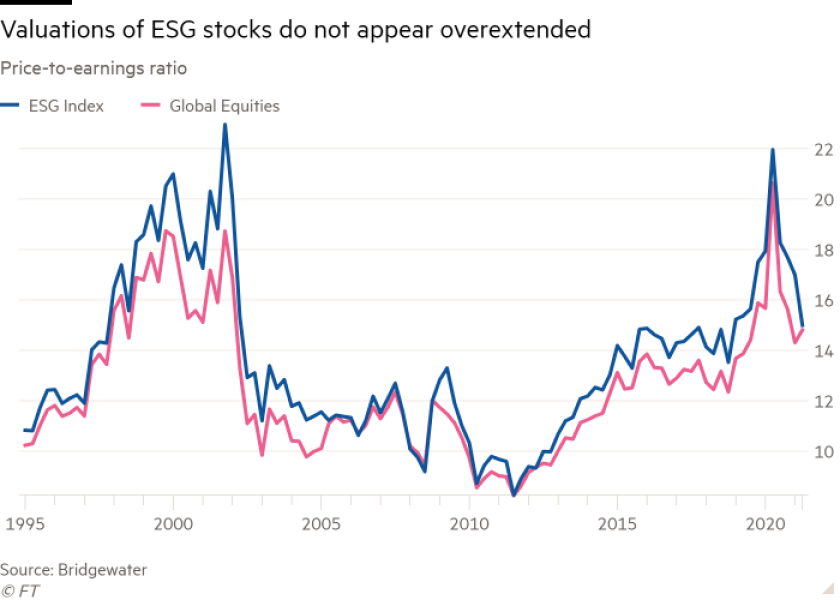

Most common ESG indices have very similar valuation characteristics to the broad market. The valuation of ESG stocks is roughly the same as a global equity portfolio. The ratio of price to average earnings over the past three years is moderate at about 14 for both.

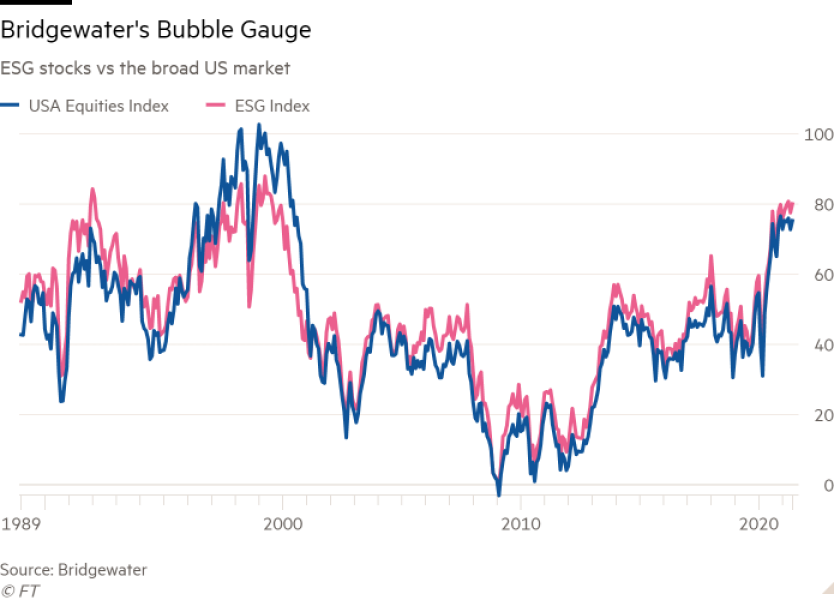

And when we assess the most popular US ESG stocks using our “bubble gauge”— a measure that combines traditional valuation metrics with factors such as the pace of new buyers, the amount of purchases funded with borrowings and whether priced-in conditions seem sustainable — only a handful of popular ESG stocks appear especially frothy.

The US ESG index looks very similar to the aggregate market, and much less frothy than stocks that have been most popular with retail investors where we think valuations are most stretched.

A few sectors that seem significantly overweight in ESG indices compared with the broader market, such as renewable electricity, have moderately higher valuations. However, these constitute only a small weighting in market benchmarks.

Why is the valuation of ESG stocks so similar to that of the overall market? One reason is that common ESG indices track the market relatively closely and intentionally avoid making large deviations.

In other words, they effectively cut out “the worst” companies rather than choosing to hold only “the very best”. As a result, these indices end up looking a lot like a typical equity allocation. They avoid directing a large portion of their capital towards a limited number of sustainability-focused stocks.

Another reason for the valuation of ESG stocks remaining in line with the market is that the shift to sustainability has been gradual — at least until recently.

We analyzed the disclosed equity holdings of a group of institutional investors that have publicly expressed significant interest in ESG, accounting for about $1.5tn in public equity assets. The moves they have made so far have been gradual and are not nearly as big as it would take to fully align with ESG indices. But a greater shift is expected.

Tobacco offers a case study. The withdrawal from the sector was long-running, but by the 2000s ESG-conscious institutions had almost no investments there. These investors have also been shifting out of the oil and defence sectors for 10 years and 20 years respectively. The shift towards “good” ESG companies such as renewable energy producers has been similarly gradual, but it now appears to be accelerating.

We suspect that large ESG flows are still ahead of us. Currently, only 4 per cent to 5 per cent of the mutual fund and ETF universe is in ESG-labelled funds, according to a Bank of America analysis of Morningstar data.

It is easy to imagine flows accelerating at an even faster pace. European investors, the vanguard of the sustainability shift, are moving their assets to ESG funds at a rate of 6 per cent to 8 per cent a year — more than twice the global average.

As allocations rise, there is likely to be big inflows and outflows out of most stocks, leading to notable price moves, particularly in sectors such as water utilities and renewable electricity.

And while today’s most common ESG indices are only modestly different from the market portfolio, investors may begin to make more ambitious changes as the sustainable investing universe continues to evolve.

Investors may choose to focus their portfolios rather than hold a large array of stocks. As there are so many stocks to choose from in the world with similar fundamental exposures to macroeconomic conditions, there is little to gain in diversification by expanding the universe of stocks beyond a modest spread of holdings. Simple portfolio maths illustrate that the initial gains from diversification — moving from one to 50 stocks — are substantial, while the later gains — moving from 50 to 500 holdings — are very small.

Investors shifting to more focused portfolios of sustainable companies would have much larger implications on relative stock prices.

With a growing share of investors prioritizing impact and sustainability, we believe there is significant room for ESG flows to run — and that sustainable investing’s largest impacts on relative stock valuations as well as the incentives facing public corporations are still ahead of us.